WHY YOUR PROFITABLE BUSINESS FEELS BROKE (THE REAL CASH FLOW STORY)

You had a profitable year.

The P&L looks great. Revenue’s up. Margins are solid.

And yet… your bank account is lower than it was 12 months ago.

What gives?

This is one of the most common (and most confusing) experiences for business owners. On paper, you’re winning. In reality, it feels like you’re treading water. Or worse, drowning.

The reason is simple, but uncomfortable:

Profit and cash are not the same thing.

And if you don’t understand the difference, your financials will feel like they’re lying to you.

Let’s start with the statement most owners live in: the Income Statement.

Revenue

– Expenses

= Net Profit

That’s it.

It tells you whether the business was economically successful during a period. But it does not tell you where the cash went or why it didn’t end up in your account.

Why?

Because many of the numbers on your income statement aren’t cash movements at all.

This is especially true if you’re running accrual-basis financials (which most growing businesses should be and very few are truly running a pure cash financial). Revenue can be recorded before cash is collected. Expenses can be recorded before cash is paid. And some expenses aren’t cash expenses at all.

Which brings us to the statement most business owners ignore: The Statement of Cash Flows.

If the income statement tells the story of performance, the Statement of Cash Flows tells the story of movement.

It answers one simple question: “What changed in the bank account during this period and why?”

At a high level, it reconciles:

Beginning cash

+/ – Cash Movements

= Ending cash

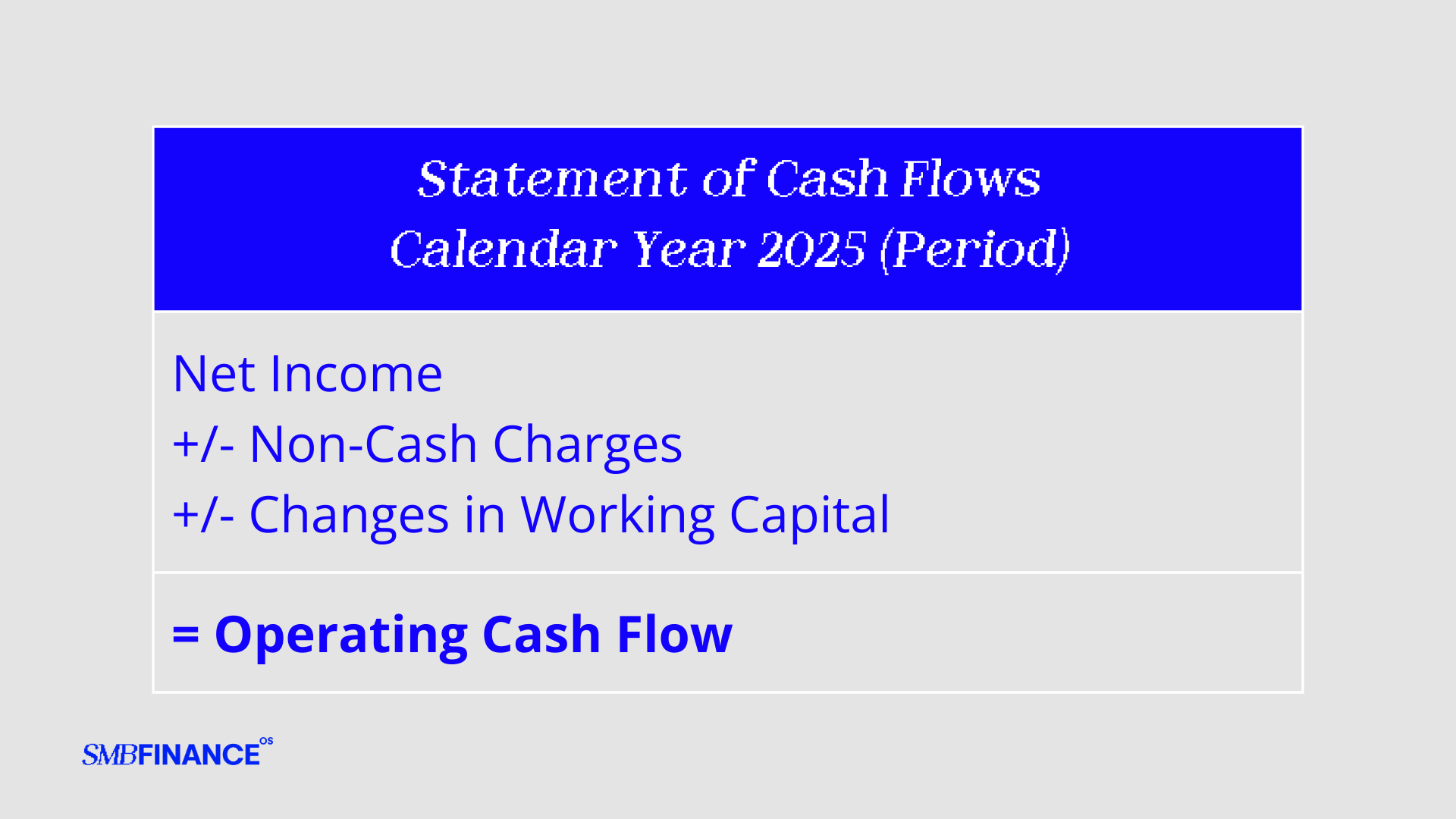

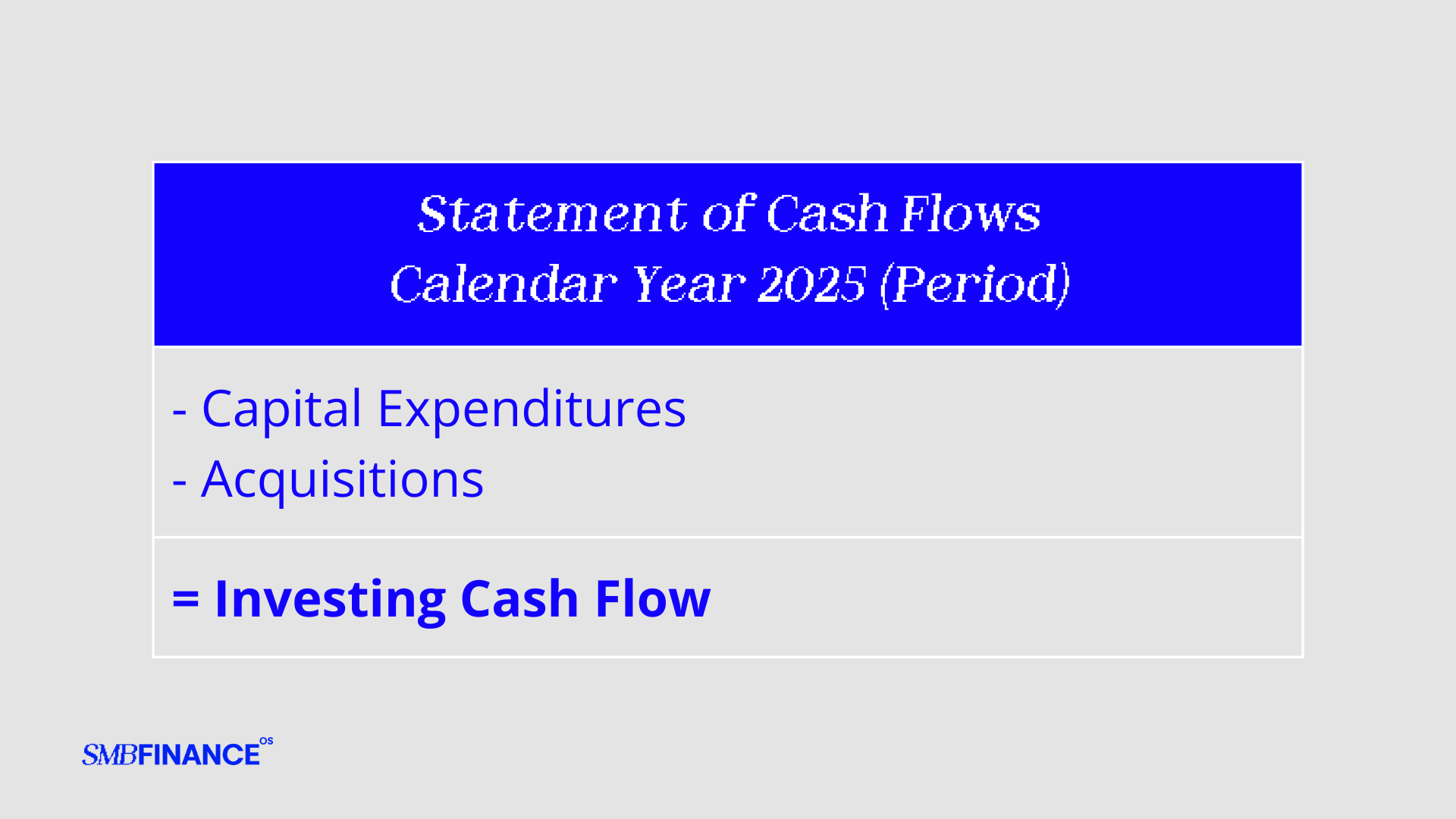

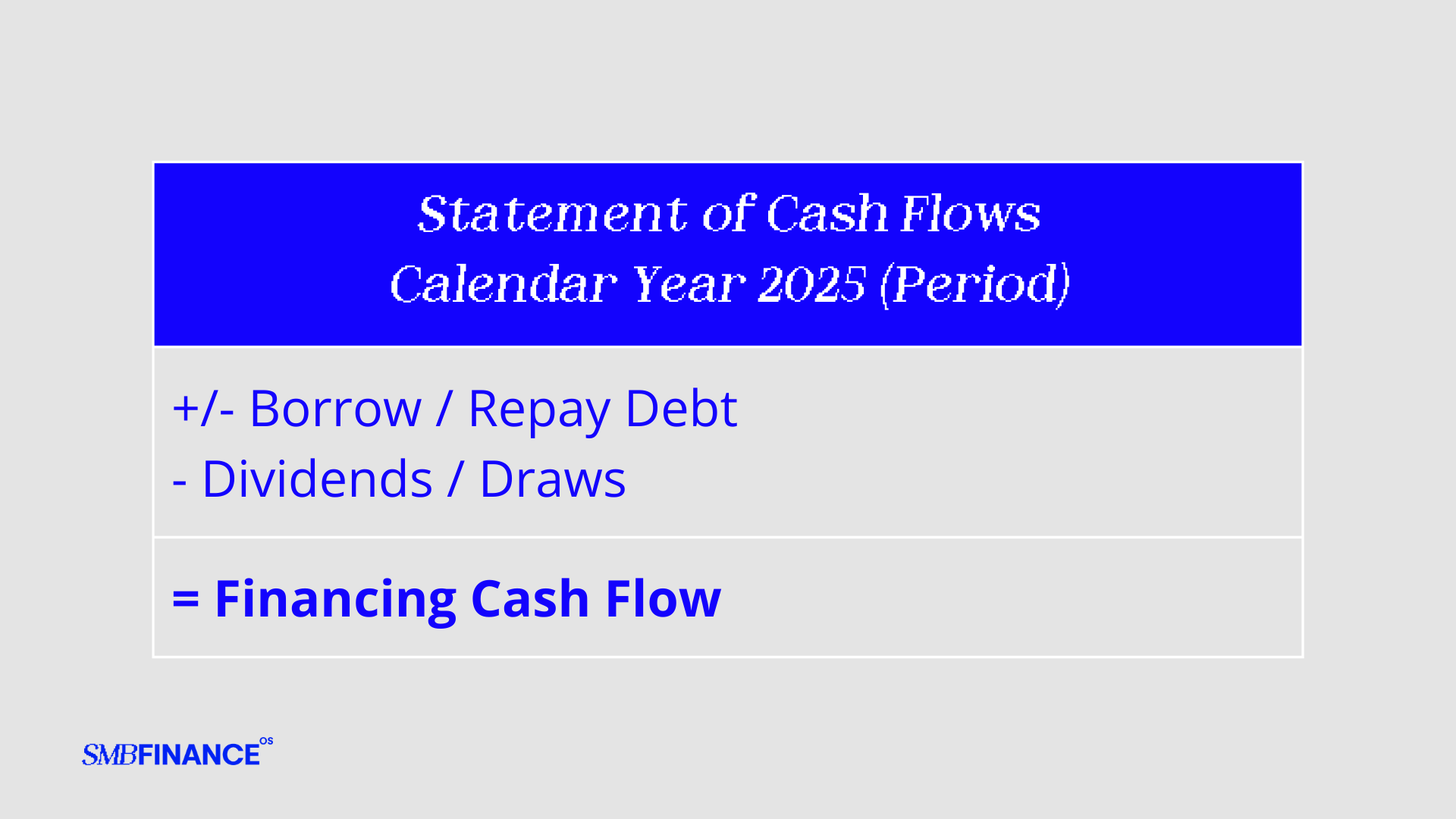

The Statement of Cash Flows puts movements into three categories: operating, investing, and financing.

But for our purposes today, we’re going to break them down into the most impactful changes in cash for you.

WORKING CAPITAL CHANGES: AR, AP, & INVENTORY

Working capital changes are part of the Operating Cash Flows. Depreciation also falls here, but is actually reduces profits… yet it’s not a “real” dollar. So this reduces profits, meaning you can actually have more cash if we look at the variable of depreciation only.

But AR, AP, & Inventory (and more specifically AR & Inventory), can cause us to have less cash than profits.

This happens because we:

- Invoice more before collecting (count revenue before dollars are received, thus AR)

- Buy inventory before selling (which is especially hard during growth periods)

- Pay vendors faster than customers pay you (again, hard when you grow)

All of these have the potential to “use” cash, which could mean profits are higher than cash received on those profits.

Especially during growth periods, this can mean you’re consuming (using more than you receive) cash even when profits look strong. This is why growth often creates a cash crunch instead of relieving it.

ASSET EXPENDITURES

Under Investing Cash Flows, there are asset expenditures. We could also talk Acquisitions, but that’s less regular, so not a focus today.

Assets are primarily:

- Equipment

- Vehicles

- Facilities

- Long-term software or systems

These purchases don’t hit your income statement immediately. Instead, they’re capitalized and depreciated over time. Depreciation is an attempt to capture the profit impact, but does not align with the cash outflow.

The cash leaves right now (unless you take out debt, which we’ll address later), which is why businesses can show strong profit while hemorrhaging cash during heavy CapEx periods.

Depreciation smooths the expense on paper, but your bank account doesn’t care.

PAYING DOWN DEBT

Debt falls in Financing Cash Flows and is an “invisible” drain on cash. Debt is split into principal and interest payments. Interest shows on the Income Statement but principal doesn’t. So in a month with a $10,000 debt payment, only part of that shows on the Income Statement.

The other part is “invisible” if you don’t look at the larger picture.

When taking out new debt, this is an “inflow” matched by an “outflow” in asset purchase or whatever the debt was for. So often you’ll see swings between Financing Cash Flows and Investing Cash Flows, which is expected.

When debt load gets large, you can have significant cash outflows here, which can strangle a profitable business. This is where debt is sneaky, and something often overlooked by green business owners. You need profits in excess of your debt obligation to continue operating.

OWNER DISTRIBUTIONS/PAYMENTS

Owner payments or distributions, often for tax purposes, come out of the Financing Cash Flows section.

This tax payment if often a function of tax profits, which means you should likely have the cash, but too often business owners spend it without realizing they’re spending money that already has a “claim” against it.

Other times, the business owner sees cash in the bank and assumes they can take it out to spend personally, reducing cash balances to pay for other uses of cash.

This is where having good systems to understand the cash you’ll need to grow, reinvest in assets, and pay debt is a key part of only taking “safe” distributions.

THE STORY OF CASH FLOW

This is not a straight forward topic and often hard for green business owners to undertstand.

So, in these cases, I like to think in terms of the story.

We have one main goal: for operating cash flow to be sufficient to cover cash needed to:

- Continue to grow (AR, AP, & Inventory)

- Reinvestment for the long-term (assets)

- Pay down debt

- Pay the owner

You can replace operating cash flows with profits and the story is similar (as profits is a derivative of operating cash flows).

When we work with business owners at Bison CFO, one of the most impactful things we do is introduce business owners to the Statement of Cash Flows.

For the first time, they’re seeing the FULL picture, instead of only part of it (when looking at Income Statement only).

When owners say, “The numbers say we’re winning, but it doesn’t feel like it,” this is why.

Long-term, healthy businesses follow a simple loop:

- Generate cash from operations

- Reinvest intentionally

- Use financing strategically

- Take excess cash out on purpose

Profit is a scoreboard.

Cash is oxygen. And oxygen (staying alive) is what we should optimize for.

WANT TO GO DEEPER?

If this resonated, I’m running a cohort called Five Days to Financial Clarity.

Over five days, we walk through:

- How money actually flows through your business

- The financial levers that really drive profit and cash

- How to fix cash flow issues at the root

- How to decide what to measure — and ignore

- How to walk away with a 90-day plan to put more cash in your pocket

If you don’t leave with more clarity and confidence, you get your money back. Period.

This runs throughout the year, so whenever you’re reading this, it’s relevant.

Join us and use the code WEBSITE to get 30% off.