HOW BUSINESSES TURN VALUE INTO CASH (AND REINVEST IT FOR THE HIGHEST RETURN)

If you added $100 of new revenue tomorrow, could you clearly explain where that money would go?

Not just “generally,” but step by step.

Who touches it. What claims it. When it actually becomes cash.

Most business owners can’t. And that gap is where confusion, stress, and bad capital decisions are born.

Businesses talk constantly about revenue and profit, but very few truly understand the flow that connects value creation to cash, and then cash to reinvestment. That missing middle is what actually determines whether a business compounds or stalls.

Let’s simplify it.

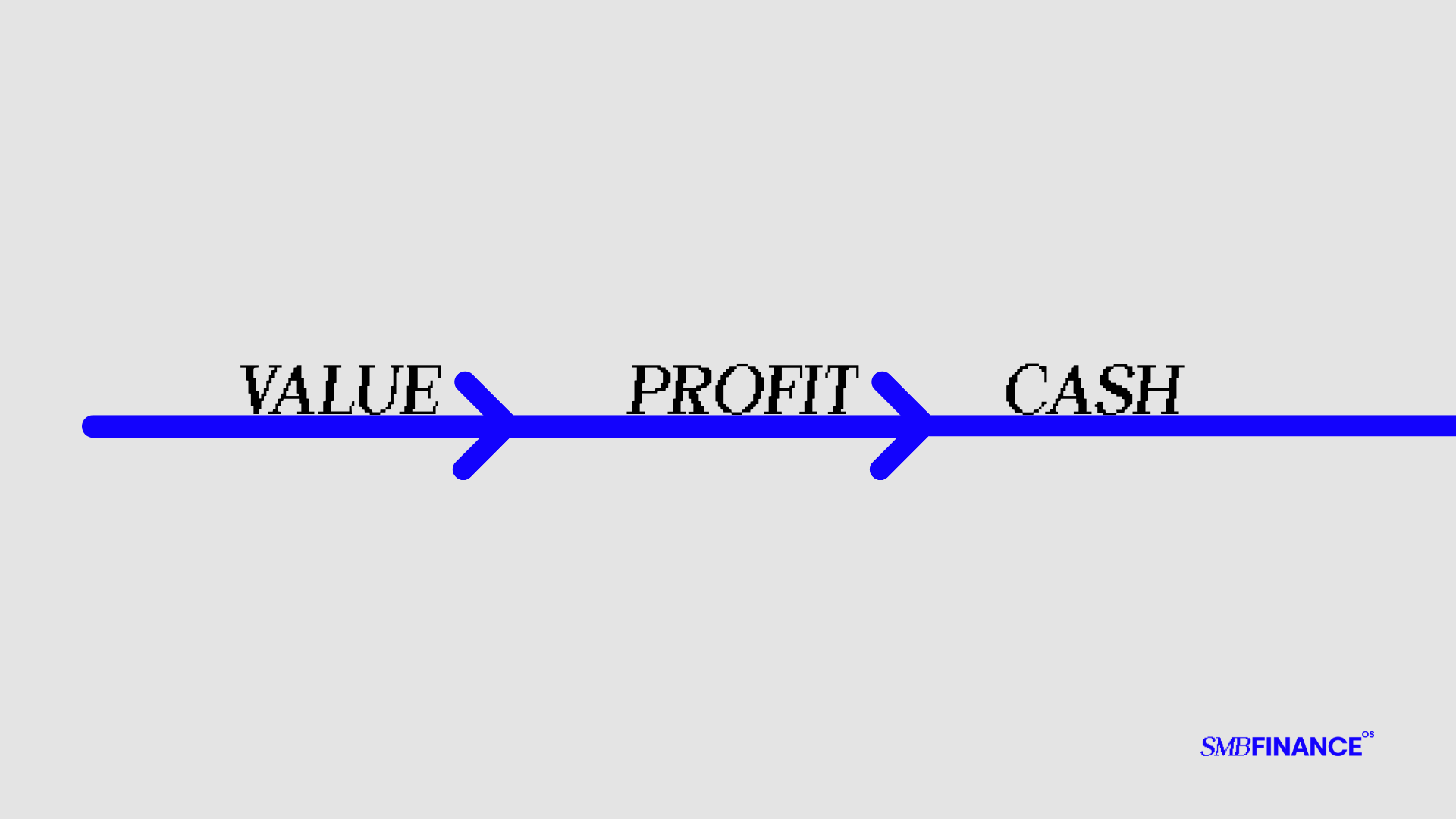

Every business runs on a basic value loop.

You create value for a customer.

That value becomes revenue when it’s sold.

It becomes profit if it’s sold efficiently.

And it becomes cash only when the timing works in your favor.

The goal is simple: start with $100 and end with $110, $120, or $130. And once the cash exists, you have a choice.

And that choice ultimately decides success or failure.

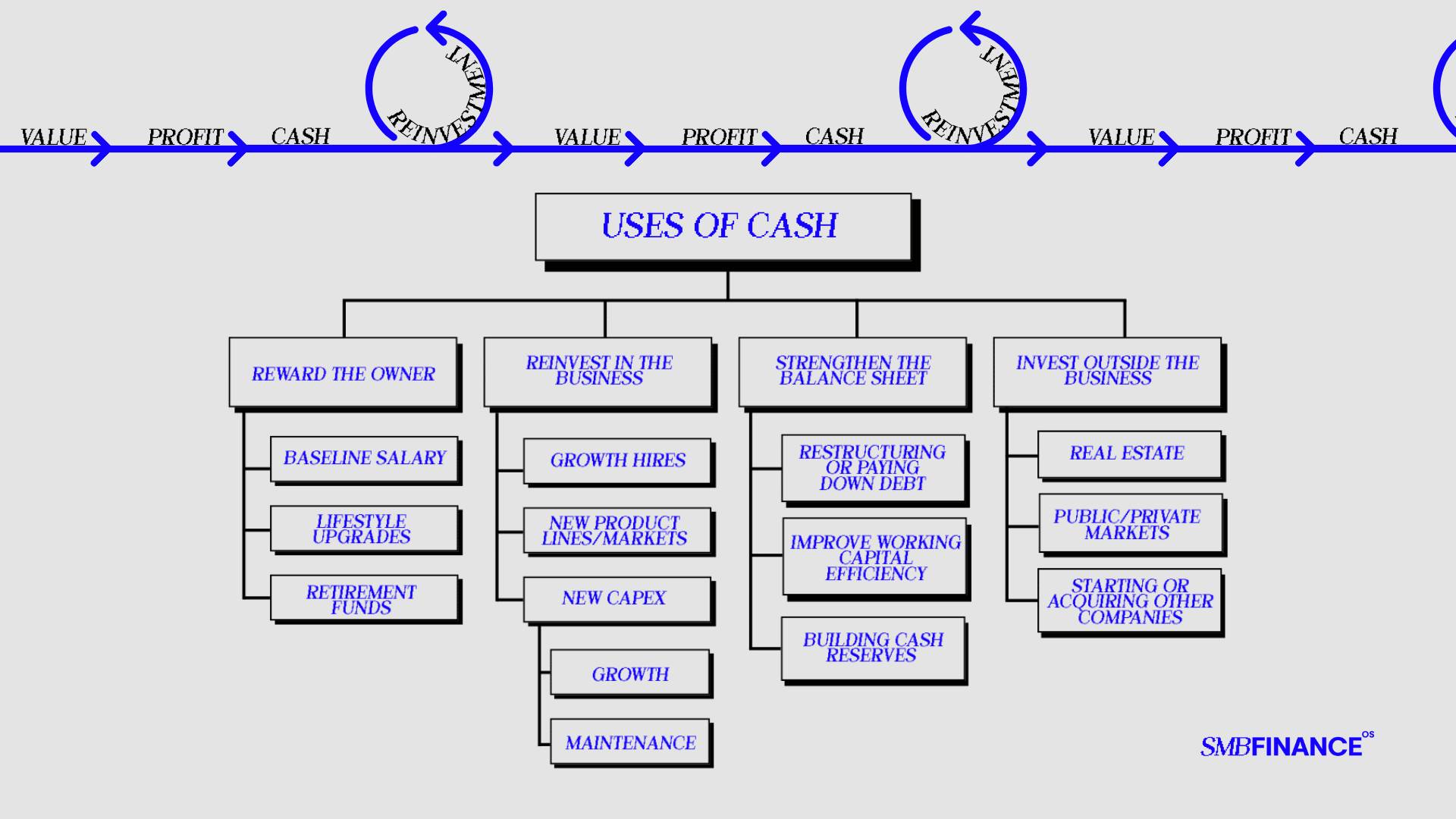

THE USES OF CASH

Cash is the output of the business, but it’s also the input to the next cycle. Once cash hits the bank, you have to decide what to do with it.

And the real goal of that decision isn’t “growth” or “safety” or “reward.”

It’s return.

Return over the long term. Return adjusted for risk. Return that supports the life you want and the business you’re trying to build.

This is where business owners often oversimplify things. They default to reinvesting everything back into the business without stopping to ask whether that’s actually the best use of capital right now.

Sometimes it is. Sometimes it’s not.

To make that decision clearer, I like to frame cash allocation into four buckets. These aren’t accounting categories. They’re decision categories.

REWARD THE OWNER

I start here intentionally, even though most people expect this to come last.

Too many owners treat themselves as the shock absorber for the business. They skip pay, delay lifestyle improvements, and push retirement “until later.” Over time, that tradeoff quietly destroys decision quality.

Rewarding the owner is about sustainability. I break it into three categories:

- Baseline salary that removes personal financial stress.

- Quality-of-life upgrades that make the sacrifice feel worth it.

- Retirement investing so your entire future isn’t trapped inside one operating company.

If you don’t take care of yourself today, it leaks into the business tomorrow. Burnout, resentment, and short-term thinking are expensive.

Stability at home creates stability in the business.

REINVEST IN THE BUSINESS

This is the most familiar bucket, and for good reason.

Reinvestment fuels growth. Hiring people. Expanding services. Entering new markets. Buying equipment. Building systems.

I like to split this into two types of spend: growth CapEx and maintenance CapEx. Growth CapEx is about expanding capacity or revenue. Maintenance CapEx is about keeping the machine running.

The mistake owners make here isn’t reinvesting. It’s reinvesting without planning. They wait until the cash is gone before realizing they needed it set aside.

Good reinvestment decisions start long before the spend happens. They require intentional cash reserves and a clear understanding of what the business will need next, not just what it wants now.

And just as important, reinvesting in the business is not always the highest-return move in every season.

Which leads to the next bucket.

STRENGTHEN THE BALANCE SHEET

Strengthening the Balance Sheet is about stability, not speed.

Paying down or restructuring debt.

Improving working capital efficiency.

Building meaningful cash reserves.

You could argue this is part of reinvesting in the business, but I separate it because the objective is different. This isn’t about growing faster, but instead increasing the probability that you survive long enough to compound.

Sometimes the highest-return decision isn’t adding more upside. It’s removing fragility.

Reducing risk creates optionality. Optionality creates leverage when the right opportunity shows up.

That’s a return most spreadsheets don’t capture well, but owners feel it every day.

INVEST OUTSIDE THE BUSINESS

This is where things get personal.

Sometimes your business is not the best place for the next dollar. And pretending otherwise doesn’t make you disciplined, it makes you biased.

Investing outside the business could mean real estate, public markets, private investments, or even personal projects. These aren’t inherently good or bad.

What matters is whether they offer a better risk-adjusted return for you at this stage of life and business.

RETURN IS PERSONAL, NOT JUST FINANCIAL

Here’s the part that doesn’t fit neatly into formulas.

You’re not just allocating capital. You’re allocating energy, attention, and risk across your lifetime.Sometimes the best “return” is reduced stress, more time, or a life that actually feels aligned with why you started the business in the first place.

Maximizing return doesn’t always mean maximizing growth. It means aligning your cash decisions with your business goals and your personal goals at the same time.

Two owners can run identical businesses and make completely different decisions here. One wants to scale aggressively. Another wants a stable, cash-generating company that supports a simple life.

Both can be right.

There’s always some judgment involved… some feel. And no one has perfect information.

But intentional decisions beat default decisions every time.

If your cash choices align with where you’re trying to go, you’re doing this right.

Businesses don’t fail because they can’t create value. They fail because they don’t convert that value into cash efficiently, or they deploy that cash poorly once they have it.

Understand the flow.

Respect the choice.

Allocate with intention.

That’s how businesses compound.