IF YOUR FINANCIALS FEEL CHAOTIC, THIS IS PROBABLY WHY (CASH VS ACCRUAL ACCOUNTING)

Are you constantly confused about your financials?

Do your margins swing wildly month to month?

Do you see high-profit months followed by low-profit months with no clear operational reason?

If that’s happening, you might have a financials problem.

Today we’re going to talk about cash versus accrual accounting and why graduating to accrual may be essential if you want to truly understand your profitability.

TYPE OF FINANCIAL STATEMENTS

We’ve talked extensively here about the three main financial statements and the core questions they answer:

- Income Statement – Are you profitable?

- Balance Sheet – Are you healthy?

- Statement of Cash Flows – Where did the cash go?

We’ve also talked about how they’re all interconnected, how net income flows into the balance sheet, and how cash movement flows from the income statement and balance sheet into the statement of cash flows.

In mature or newer business owners, focus solely on the income statement, often ignoring the other two. Since they’re running mostly cash financials, this isn’t a huge deal as all activity is represented on that income statement. But once more complexity starts creeping in the business, the financials can become a huge mess.

This isn’t strictly cash versa cruel. When you look at the landscape, there are really four types of prepared financial statements:

- Cash

- Accrual

- Modified Cash

- Tax

CASH FINANCIALS

Cash in. Cash out.

No accounts receivable.

No accounts payable.

No inventory recorded.

You’re essentially mirroring your Income Statement and bank account.

ACCRUAL FINANCIALS

Revenue when earned. Expenses when incurred, not when cash moves.

This requires:

- Tracking receivables and payables

- Recording inventory

- Spreading prepaid expenses

- Recognizing liabilities properly

- Using the balance sheet as a real operating tool

We’ll break this down further in a minute.

MODIFIED CASH FINANCIALS

This is where most small businesses actually live.

They’ll record revenue when earned and match the cost of goods sold expense to that revenue, but when it comes to overhead expenses they record those when paid.

So you’ll record inventory, accounts payable, and accounts receivable but ignore all accruals.

This often means you’re recording depreciation at year-end and had unrecorded obligations (like insurance, bonuses, and other prepaid expenses).

This is not bad and often the right path for many small businesses but it’s easy to get off track here and end up with unrecorded obligations that skew your original plans.

This results in your numbers only partially reflecting reality.

TAX BASIS FINANCIALS

This is the most misunderstood category. Many owners go to their CPA and say, “We need financials.” They get financials and then wonder why they struggle to make decisions off of them.

Your CPA’s job is tax compliance. They’re giving you tax-focused financials not decision-making focused financials.

Their financials are not optimized for understanding margins, managing teams, or making capital decisions.

And then owners wonder why they can’t get anything useful out of them.

CASH VS ACCRUAL: WHAT DOES IT MEAN?

At its core:

Cash basis:

- Revenue when cash is received

- Expense when cash is paid

Accrual basis:

- Revenue when earned

- Expense when incurred

This is oversimplified but also the basic principle. The best way for us to work through this is to go through some examples.

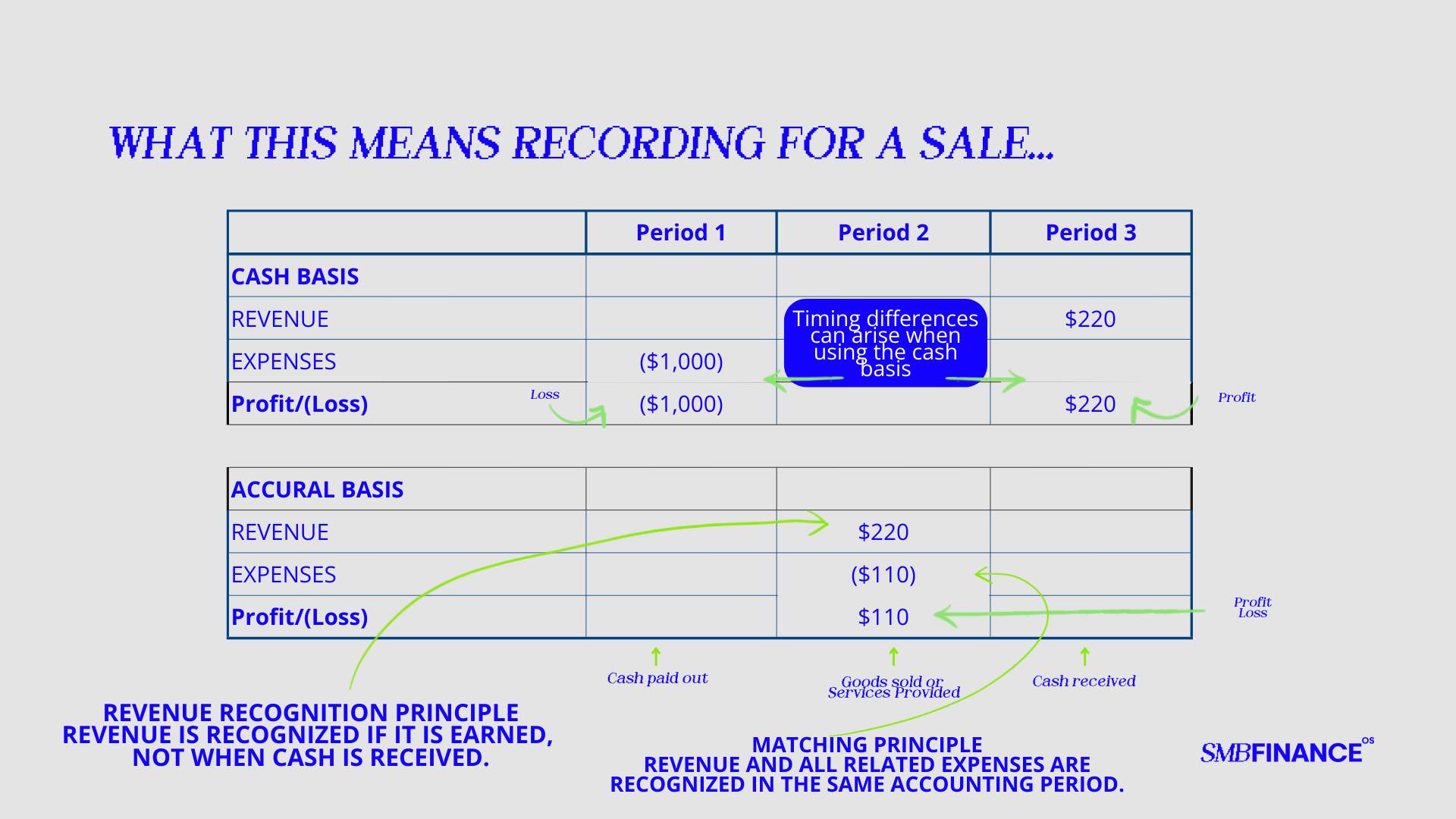

EXAMPLE 1: INVENTORY

On April 30th, you buy 100 units of product for $1,000.

On May 20th, you sell 11 units, but you don’t get paid until June 11th.

On Cash Basis:

- April: $1,000 expense

- June: Revenue recorded when payment arrives

- No inventory is ever shown

- The full cost hit in April

Your income statement shows:

- April: Big loss

- June: Revenue with no related expense

- You appear unprofitable overall, even though you made money on what you sold

On Accrual Basis

- April 30th: Inventory recorded as an asset

- May 20th: Revenue recognized when sold

- Cost of goods sold recorded only for the 11 units sold

- Remaining 89 units stay on the balance sheet as inventory

In accrual revenue and costs line up. In cash it’s strictly based off when cash comes in and out of the business.

The curl allows you to see your true gross margin on that sale… you made $110. In the cash basis financials, that fact is obscured.

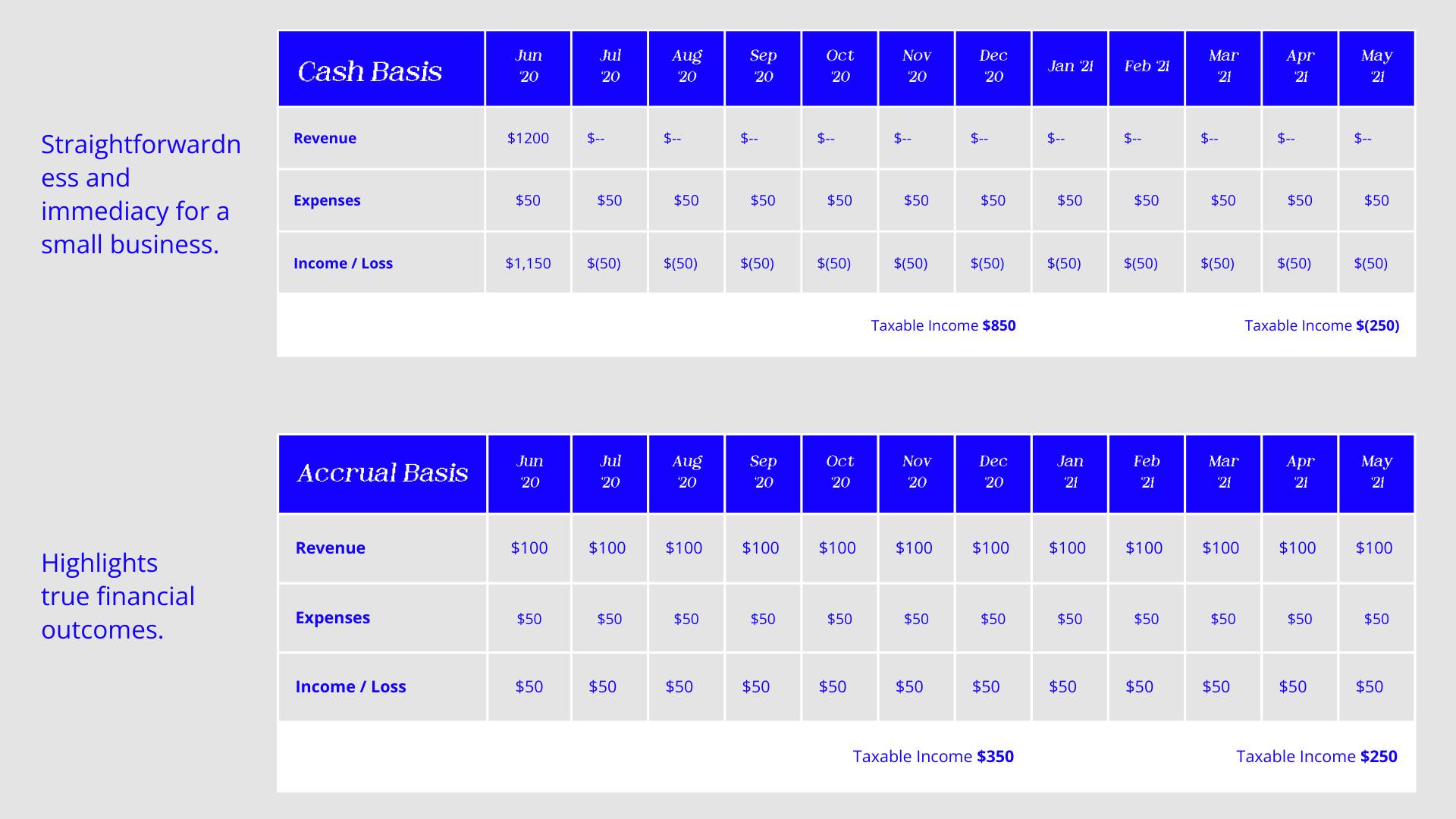

EXAMPLE 2: SUBSCRIPTION REVENUE

Let’s say a customer pays you $1,200 upfront on June 1st for a 12-month service contract.

You pay $50 per month for chemicals to fulfill that service.

On Cash Basis

June:

- $1,200 revenue

- $50 expense

Looks incredible.

July–May:

- $50 expense each month

- No revenue

Now it looks like you’re losing money.

Operationally, nothing changed, but your financials are telling two completely different stories.

On Accrual Basis

You recognize:

- $100 revenue each month

- $50 expense each month

Now your profitability is stable and consistent.

You’re matching revenue with the expense required to generate it.

That’s called the matching principle and it’s foundational to accrual accounting.

Since the revenue happened in June under cash, you show huge profits for that year and have lost for the next year. On a cruel you show smaller profit on the first year and a profit on the second year and distribute the profit more evenly across the service being performed.

WHY THIS MATTERS FOR YOUR BUSINESS

Margins are the heartbeat of your business.

If your margins are swinging wildly because of:

- Inventory timing

- Prepaid expenses

- Customer deposits

- Receivable collections

- Bonus payouts

- Capital purchases

…then you don’t actually understand your business model. You’re reacting to noise.

Accrual accounting:

- Levels out artificial swings

- Makes gross margin meaningful

- Allows real trend analysis

- Helps you evaluate managers fairly

- Supports better pricing decisions

- Improves capital planning

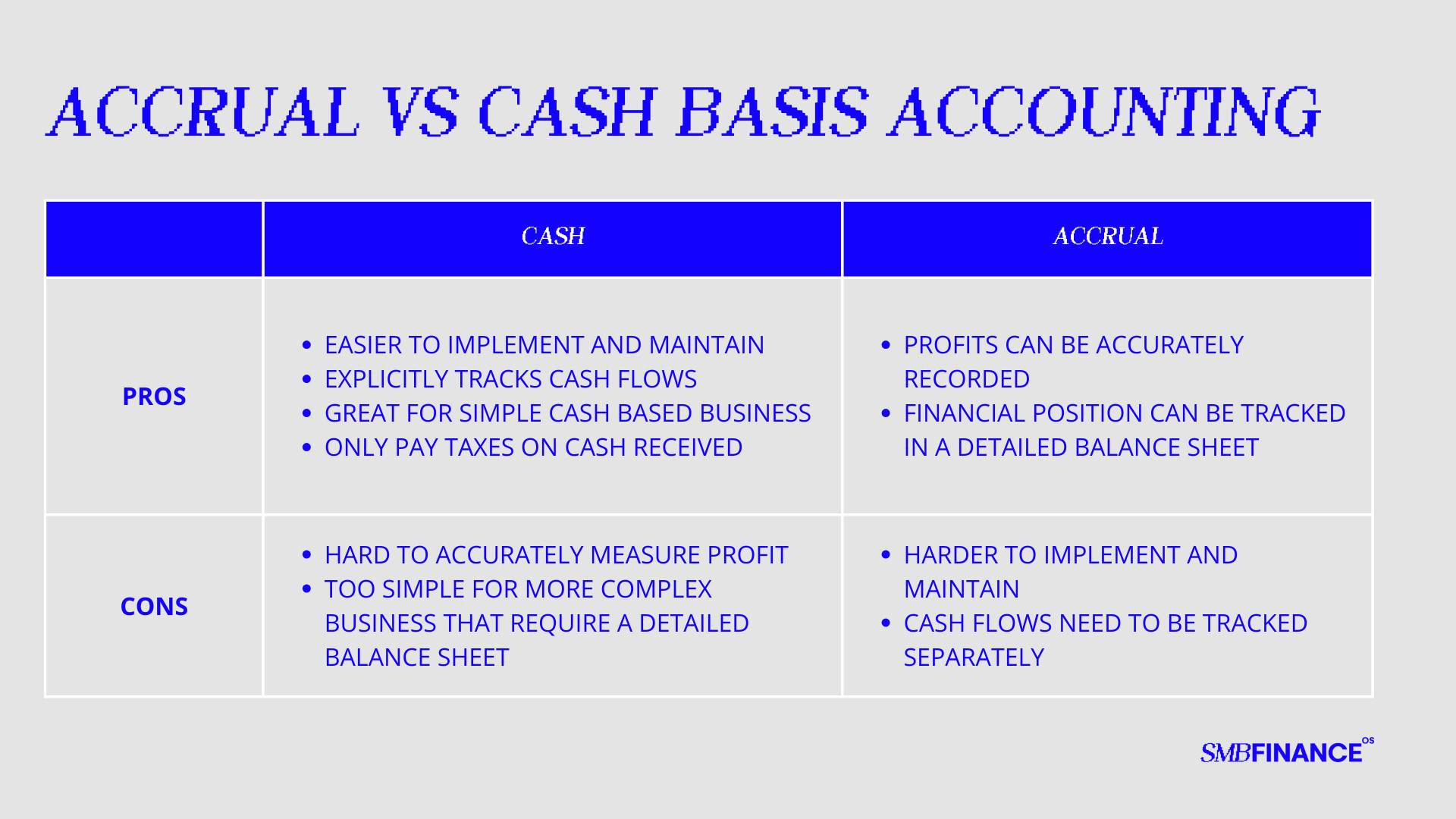

Cash basis is simple, but simple does not mean accurate or actionable.

Now, lets be clear: accrual does not eliminate the need to track actual cash movement in your business. If anything, it can make it clearer, though.

In fact, once you move to accrual:

- The Income Statement measures performance.

- The Balance Sheet measures health.

- The Statement of Cash Flows explains timing.

- Cash forecasting becomes essential.

In my view this is actually great because you start to have to use the right tool for the job of understanding cash movement. That’s maturing!

WHEN SHOULD I SWITCH TO ACCRUAL?

There are pros and cons to each. For some businesses it makes sense to stay on cash basis even for internal reporting.

But sometimes complexity in the business grows. Financials are needed to fully understand that new complexity.

You should strongly consider accrual if:

- Your margins swing wildly month to month.

- You carry inventory.

- You invoice before getting paid.

- You receive deposits before doing the work.

- You have meaningful prepaid expenses.

- You are managing performance-based compensation.

- You are doing capital planning.

- You are considering selling, acquiring, or raising capital.

- You have debt and need balance sheet clarity.

- You keep saying, “We’re profitable, but I don’t understand where the cash is going.”

Accrual gives you a deeper understanding of:

- Where profit is created

- Where it’s being reinvested

- Where cash is tied up

- What obligations exist

- Whether your margins are real

Most businesses live somewhere between pure cash and pure accrual and that’s completely fine.

It’s most important that you truly understand your margins, manage performance intelligently, and lead strategically.

Also to be clear, your tax accountant is still going to prepare their tax financials but we don’t want to get into the trap of just accepting their numbers meant for their tax-focused purposes. We want our financials to facilitate us in our strategic decision-making and can help us grow and mature our business.

Yes, it’s more complex. But it’s also more honest.

If you have questions about how to implement this in your business, I’d love to talk. Just reply to this email and we can schedule a call.