YOU'RE NOT BROKE, YOUR CASH IS JUST STUCK (CASH CONVERSION CYCLE EXPLAINED)

Most business owners don’t actually have a profit problem.

They have a timing problem.

The business is profitable on paper, but the bank balance never seems to reflect it. Payroll feels tight. Inventory purchases are stressful. Taxes show up like a surprise, even though they come every year.

This disconnect usually has one root cause: cash is trapped inside the business cycle.

That’s where the Cash Conversion Cycle comes in.

This may be one of the most important metrics in your business, because it determines how fast you can grow and how stressful that growth will feel.

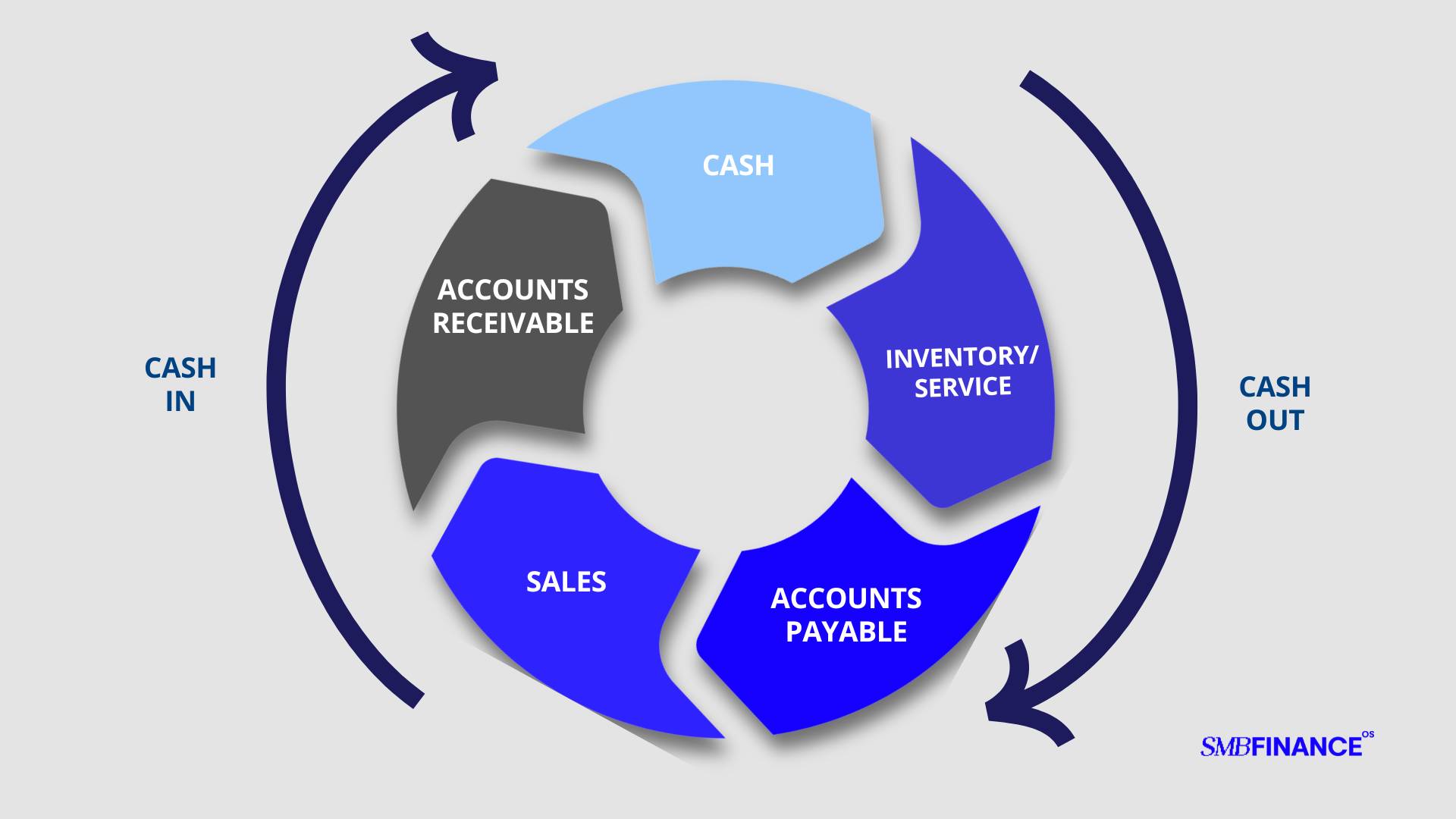

THE CASH LOOP

Every business starts and ends with cash. The goal is simple: turn cash into more cash.

But between those two points, cash has to move through a loop.

You spend money first. That might be inventory if you sell products. It might be payroll, contractors, or materials if you sell services.

That spending creates an obligation. Sometimes you pay immediately. Sometimes you get terms and pay later.

Then you sell something. That sale creates revenue, but not always cash. If you invoice customers, you’re holding a promise to be paid in the future.

Eventually, cash comes back into the business. That cash is then used to repeat the cycle.

The question that matters is this: how long does that loop take?

WHAT THE CASH CONVERSION CYCLE ACTUALLY MEASURES

The Cash Conversion Cycle answers one question:

“How many days pass between spending a dollar and getting that dollar back?”

It’s made up of three components:

- Days Inventory Outstanding (DIO): how long inventory or work-in-process sits before it’s sold

- Days Sales Outstanding (DSO): how long it takes to collect cash after a sale

- Days Payable Outstanding (DPO): how long you wait to pay vendors

Cash Conversion Cycle = DIO + DSO − DPO

It’s three formulas in one… easy right? Yeah, I get it, it’s hard.

But when it comes down to it, it really isn’t that complicated. How long does it take from initial commitment to inventory to turn that into a sale?

A longer cycle means cash is tied up longer. A shorter cycle means cash moves faster. And the faster your cash cycles, the easier it is to fund growth internally.

WHY LONG CYCLES QUIETLY STRANGLE GROWTH

We worked with a product business that felt like it was constantly drowning in cash pressure despite strong demand. When we mapped their cycle, the problem became obvious.

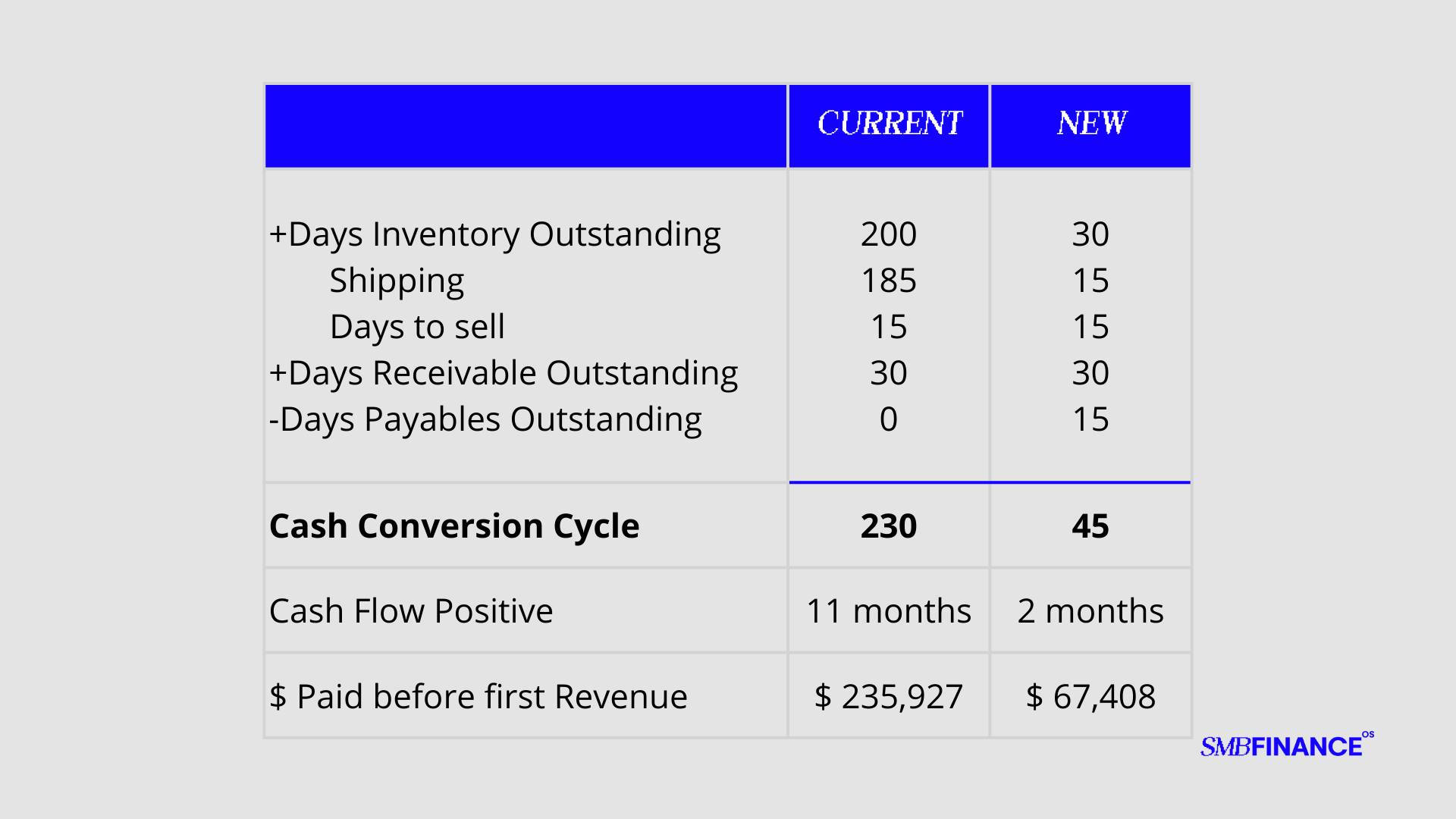

It took them about 200 days from ordering inventory to selling it. Most of that time was lead time from overseas suppliers. Once the inventory arrived, it sold relatively quickly.

On top of that, some customers paid immediately, but others were on terms and slow to pay. On average, receivables added another 30 days.

And vendors required payment upfront.

That meant their cash conversion cycle was roughly 230 days.

They had to fully fund almost 11 months of activity before seeing cash over and above their dollar spent on inventory.

As they grew, the problem got worse. Growth required more inventory, which required more upfront cash. Profit didn’t matter if the business couldn’t survive the wait.

THE LEVERS THAT CHANGED EVERYTHING

The breakthrough didn’t come from “working harder” or “selling more.” It came from attacking the cycle itself.

First, they challenged supplier assumptions. They found a new supplier that could get inventory to their warehouse in 15 days and didn’t require payment until it landed. This effectively wiped out the previous 185 days of shipping. That alone collapsed inventory days from 200 to around 30.

Second, they improved collections discipline. No new fancy systems. Just tighter follow-up and clearer rules around who actually got terms. Over time, DSO dropped from the mid-30s to about 20 days.

The result?

Their cash conversion cycle dropped from 230 days to roughly 45 days.

That single shift reduced the amount of upfront cash required to operate from over $230,000 to under $70,000. The business didn’t suddenly become more profitable. It became liquid.

That liquidity changed everything. The owner could take distributions. Growth no longer felt dangerous. Cash stopped being a daily source of stress.

THIS ISN’T JUST FOR PRODUCT BUSINESSES

Service businesses often assume this doesn’t apply because they don’t carry inventory. That’s a mistake.

Inventory can be replaced with time.

How long does it take between doing the work and invoicing?

How long between invoicing and getting paid?

When do you pay payroll or contractors relative to delivery?

If you do the work on April 1st, pay payroll on April 10th, invoice on April 30th, and get paid on May 28th, your cash is tied up for weeks. That’s still a cash conversion cycle, just with different labels.

WHAT’S NEXT

I want to let you in on a cycle: negative cash conversion cycles are real. Some businesses are able to collect cash before ever incurring any cost.

That’s when growth creates cash instead of consuming it.

It doesn’t mean the business is easy to run. Fulfillment still matters. But cash stress disappears from the growth equation.

But know, you may think your cycle is fixed, but it’s not. There are always improvements to make.

This week, calculate your cash conversion cycle. Don’t overthink it. Use averages. Directional accuracy is enough.

Then ask three questions:

- Where does cash sit the longest?

- What assumptions have we never questioned?

- Which lever could realistically move in the next 90 days?

You don’t need to fix everything at once. One small improvement can unlock more cash than a big increase in profit.

Cash problems rarely mean you’re failing.

More often, it just means your cash is stuck.

Free it, and the business breathes again.

If you want help doing this and are interested in increasing profits and keeping more cash in your business, join us for our next workshop 5 Days to Financial Clarity.

Over five days, we walk through:

- How money actually flows through your business

- The financial levers that really drive profit and cash

- How to fix cash flow issues at the root

- How to decide what to measure — and ignore

- How to walk away with a 90-day plan to put more cash in your pocket

If you don’t leave with more clarity and confidence, you get your money back. Period.